Michigan Boat Sales Tax: The Basics

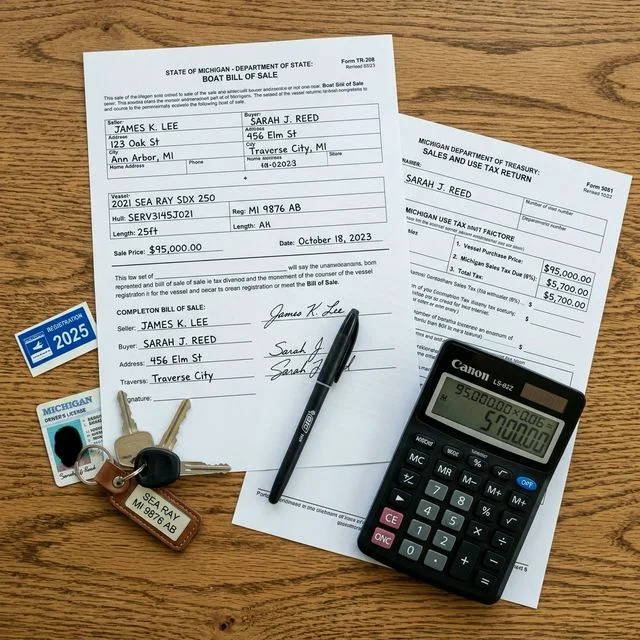

Michigan levies a flat 6% sales tax on the purchase of all watercraft. This rate applies statewide with no local or county add-on taxes — a simplicity advantage that many boat buyers appreciate compared to states with variable local tax rates.

Unlike states such as Georgia, Ohio, or Indiana that charge annual property or excise taxes on boats, Michigan imposes no recurring annual tax on registered watercraft. Once you pay the one-time 6% sales or use tax at the time of purchase, your ongoing costs are limited to the 3-year registration renewal fee.

This makes Michigan one of the most financially attractive states for long-term boat ownership in the Great Lakes region. For complete registration costs, see our Michigan boat registration guide.

How Michigan Boat Sales Tax Is Calculated

The 6% tax is applied to the full purchase price of the vessel. For dealership purchases, the dealer collects the tax at the time of sale. For private-party sales, the buyer pays the use tax when titling and registering the boat at a Secretary of State (SOS) office.

Here are several examples showing how the tax applies to different boat purchases:

| Boat Type | Purchase Price | 6% Tax | 3-Year Reg Fee | Total Upfront |

|---|---|---|---|---|

| Used fishing boat (16 ft) | $8,000 | $480 | $48 | $528 |

| Pontoon boat (22 ft) | $35,000 | $2,100 | $115 | $2,215 |

| Cabin cruiser (30 ft) | $85,000 | $5,100 | $168 | $5,268 |

| Luxury yacht (45 ft) | $250,000 | $15,000 | $280 | $15,280 |

For used boats purchased from a private seller, the Michigan Department of Treasury may assess use tax based on the fair market value — not the declared purchase price — if it appears the stated price is significantly below market value. Keep your bill of sale and any supporting documentation of the boat's condition to justify a lower price if needed.

Sales Tax vs. Use Tax: What's the Difference?

Michigan distinguishes between sales tax and use tax, though the rate for both is 6%:

Sales tax is collected by Michigan-based dealers and retailers at the point of sale. When you buy a boat from a licensed Michigan dealer, the sales tax is automatically included in the final invoice and remitted to the state by the dealer.

Use tax applies when you purchase a boat outside Michigan and bring it into the state for use or storage. The use tax rate is also 6%, and it's collected by the Secretary of State when you register and title the boat in Michigan. The key purpose of the use tax is to prevent buyers from evading Michigan sales tax by purchasing boats across state lines.

If you paid sales tax in another state on the same boat, Michigan provides a tax credit for the amount already paid. You only pay the difference, if any. For example, if you bought a boat in Wisconsin and paid 5% sales tax, you would owe Michigan only the 1% difference when registering the boat here.

Tax Exemptions and Special Situations

Several situations offer full or partial exemption from Michigan's 6% boat sales/use tax:

| Exemption | Details |

|---|---|

| Family transfers | Transfers between immediate family members (parent, child, sibling, spouse) may qualify for use tax exemption |

| Inheritance | Inherited watercraft are exempt from use tax; proof of inheritance required |

| Tax credit from other states | Sales tax paid in another state is credited toward Michigan use tax (pay only the difference) |

| Commercial vessels | Boats used exclusively for commercial purposes may qualify for certain exemptions |

| Government & nonprofit | Vessels owned by government entities or qualified nonprofits are exempt |

To claim an exemption, bring documentation (e.g., proof of relationship for family transfers, death certificate and will for inheritance) to the SOS office when registering the boat. The burden of proof is on the buyer to demonstrate eligibility.

The No Annual Tax Advantage

One of Michigan's biggest financial advantages for boat owners is the absence of any annual property or excise tax on watercraft. Many states charge yearly taxes that can add up to significant long-term costs. Here's how Michigan compares:

Over a 5-year ownership period, Michigan boat owners can save $1,000-$2,500 or more compared to neighboring states that charge annual property or excise taxes. This advantage grows with higher-value boats and longer ownership periods.

This cost savings makes Michigan particularly attractive for high-value boat purchases. Many boaters in Ohio and Indiana who own lakefront property in Michigan choose to register their boats in Michigan specifically to take advantage of this tax structure (provided they meet the residency or primary use requirements).

Buying a Boat Out of State: Use Tax Rules

Cross-border boat purchases in the Great Lakes region are common, especially at dealerships near state lines. Here's what Michigan buyers need to know about use tax on out-of-state purchases:

If you buy from an out-of-state dealer: The dealer may or may not collect Michigan sales tax. If they don't, you will owe 6% use tax when you register the boat at a Michigan SOS office. Credit is given for any sales tax paid in the seller's state.

If you buy from a private seller in another state: No sales tax is collected at the time of sale. You will owe the full 6% Michigan use tax when registering.

The "tax credit" calculation: If you paid 5% sales tax in Wisconsin on a $30,000 boat ($1,500), and Michigan's rate is 6% ($1,800), you would owe only $300 in Michigan use tax. If you paid 7% in Indiana ($2,100), you would owe $0 in Michigan — but you do not receive a refund for the excess tax paid.

Pro tip: Save all receipts and documentation of sales tax paid in other states. You will need to present this at the SOS office to claim your tax credit. Use our fee calculator to estimate your total costs.

Pending Legislation: Senate Bill 0776 (2026)

In February 2026, Michigan Senate Bill 0776 was introduced proposing changes to the use tax on recreational watercraft. Key provisions of this bill include:

- Exemptions for certain recreational watercraft from use tax

- Even with exemptions, use tax would still apply to the first $18,000 of the tax amount due

- Targeted at encouraging large boat purchases and marina industry growth in Michigan

As of March 2026, this bill has been introduced but not yet passed. Boat buyers should check the current status of this legislation before making major purchases. If enacted, it could meaningfully reduce the tax burden for high-value boat purchases in Michigan.

Michigan vs. Neighboring States: Tax Comparison

Understanding how Michigan's boat tax structure compares to neighboring Great Lakes states can help you make an informed purchasing decision:

| State | Sales Tax Rate | Local Add-On | Annual Boat Tax | Tax Cap |

|---|---|---|---|---|

| Michigan | 6% | None | None | None |

| Ohio | 5.75% | Up to 2.25% | Varies by county | None |

| Wisconsin | 5% | Up to 0.6% | None | None |

| Indiana | 7% | None | Yes (Excise Tax) | None |

| Minnesota | 6.875% | Varies | None | None |

Michigan's combination of a moderate sales tax rate (6%), zero local add-on taxes, and no annual boat tax creates an attractive overall tax picture. While Wisconsin has a lower base rate (5%), Michigan's no-tax-cap simplicity and zero annual tax make it competitive for boats of all sizes. For a full 50-state comparison, visit our cost-by-state comparison page.

How to Pay Your Boat Sales or Use Tax

Dealer purchases: Sales tax is collected and remitted by the dealer at the point of sale. You do not need to do anything additional — the dealer handles all tax paperwork.

Private-party purchases: Use tax is paid at the time of title and registration at a Michigan Secretary of State office. Acceptable payment methods include personal check, money order, credit/debit card, or cash. A receipt is provided and becomes part of the title file.

Out-of-state purchases: Present your out-of-state sales tax receipt at the SOS office to receive a credit. If you cannot prove sales tax was paid, the full 6% use tax will apply. For more details on the title transfer process, see our Michigan title transfer guide.

Common Tax Mistakes Michigan Boat Buyers Make

Avoid these costly errors when handling Michigan boat sales tax:

- Under-reporting purchase price: Michigan may assess use tax based on fair market value if the stated price is suspiciously low — this can result in additional tax plus penalties

- Losing out-of-state tax receipts: Without proof of sales tax paid in another state, you lose the tax credit and pay the full 6%

- Assuming no tax on used boats: Michigan charges use tax on all private-party sales, including used boats — there is no exemption for used vessels

- Confusing sales tax with registration fees: The 6% tax and the 3-year registration fee are separate charges paid at different points in the process

- Forgetting the title fee: In addition to tax and registration, boats requiring titles incur a $5 (standard) or $10 (instant) title fee

Taking the time to understand Michigan's tax structure before your purchase can save you money and avoid surprises at the SOS office. Use our nationwide sales tax guide for broader context.

Frequently Asked Questions

What is the sales tax rate on boats in Michigan?

Does Michigan charge an annual property tax on boats?

Do I owe Michigan use tax if I bought my boat in another state?

Are family boat transfers exempt from sales tax in Michigan?

How does Michigan boat tax compare to Ohio and Indiana?

Sources

- Michigan Department of Treasury — Sales and Use Tax (https://www.michigan.gov/treasury)

- Michigan Secretary of State — Watercraft Registration (https://www.michigan.gov/sos/vehicle/boat)

- Michigan Legislature — Senate Bill 0776 (2026)

This information is provided for reference purposes only. While we strive to keep data accurate and up-to-date, registration requirements, fees, and regulations may change without notice. Always contact your state's official registration agency for the most current and authoritative information before making any decisions.